The following are excerpts from “Local Governments Responding: The Housing Crisis in North Carolina, a report recently issued by NCLM and the N.C. Association of County Commissioners, and based on survey data taken from the fastest growing planning jurisdictions in the state. Please utilize these findings to help make the case that local governments are taking positive steps to address housing affordability in North Carolina, and that their actions to lead on this critical issue require local authority and flexibility.

INTRO

North Carolina, like much of the rest of the country, faces a crisis in housing affordability. Few people question that is the case, as the median home price in the state rose by 25% in 2021. Added to that fact is that more and more renters in North Carolina are cost-burdened, paying more than 30% of their income in rent.

Housing affordability has been an issue that the state’s most urbanized areas have been facing and addressing for years, but finding affordable places to live is increasingly a problem in communities of all sizes. Outside of places like Raleigh and Charlotte, tourism communities in the mountains and at the coast have especially struggled in recent years to meet the housing needs of a workforce that allows local economies to function. And as urban centers have become more attractive, booming suburban communities have also seen housing costs rise.

The cause of the rise in the cost of housing is complex. It encompasses everything from a 60-year trend of urbanization to labor shortages to supply chain disruptions created by the COVID-19 pandemic. Nonetheless, some critics have wanted to place the blame on cities and counties themselves, without recognizing that these same communities, with their job growth and attractive amenities, are simply facing the consequences of their own success. Land-use policies, as well as building approval processes, have come under scrutiny as the housing affordability crisis has escalated.

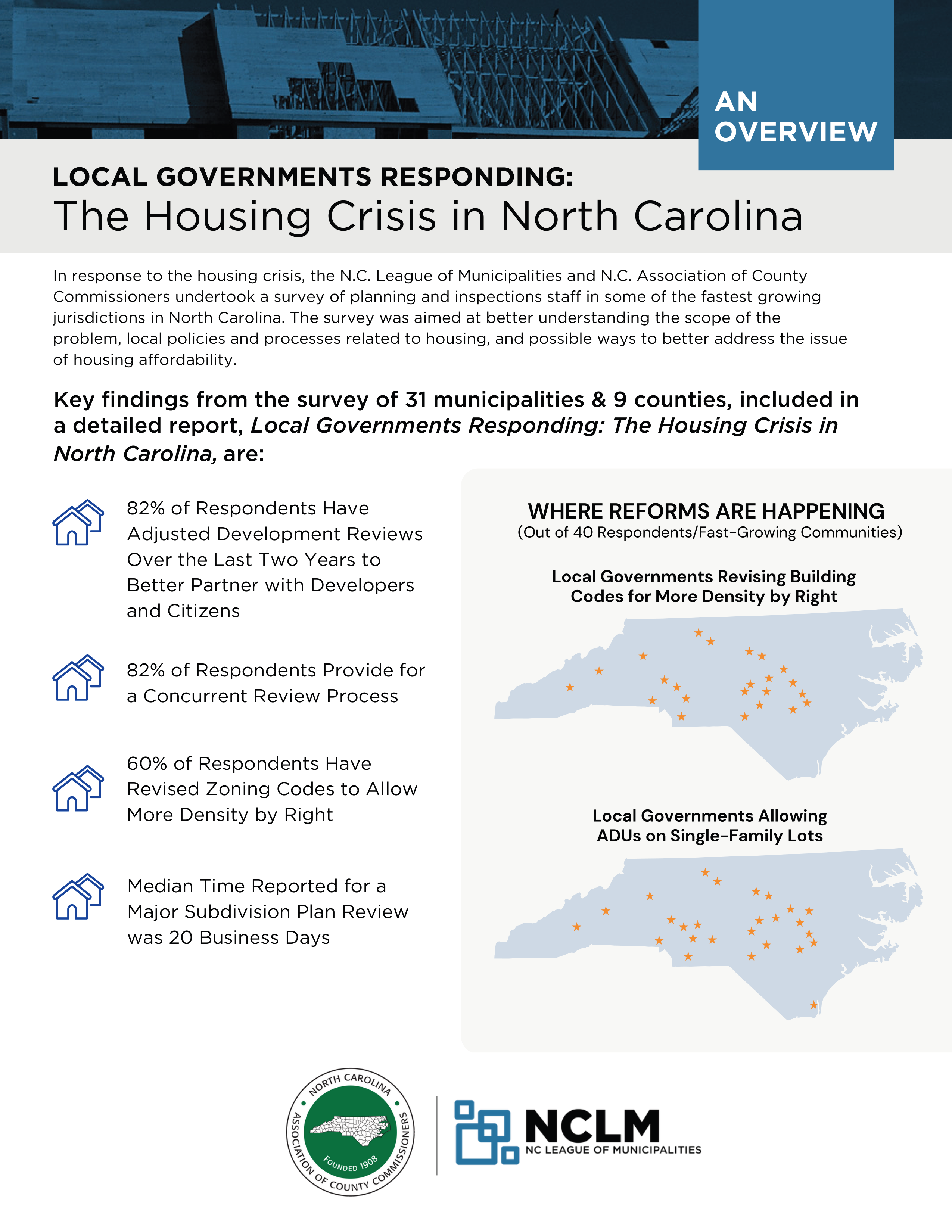

In response to the housing crisis, the N.C. League of Municipalities and N.C. Association of County Commissioners undertook a survey of some of the fastest growing jurisdictions in North Carolina to better understand the scope of the problem, local policies and processes related to housing, and possible ways to better address the issue of affordable housing. Thirty-seven local jurisdictions (building inspections and planning departments), representing 31 municipalities and nine counties, responded. These jurisdictions ranged in size from the City of Raleigh and County of Mecklenburg to several smaller municipalities in fast-growing Brunswick County, such as Shallotte and Oak Island. They also included three joint municipal-county departments, Durham-Durham County, Sanford-Lee County and Winston-Salem-Forsyth County.

This report examines those findings, delves more deeply into the causes of the housing affordability crisis, and looks at ways that are or could be utilized to help North Carolinians better accomplish the goal of home ownership and finding housing that fits their budget.

A CRISIS IN AFFORDABILITY

As noted earlier, the housing affordability crisis in North Carolina has become increasingly broad, affecting a range of communities. Even before the economic fallout associated with the COVID-19 pandemic, 45% of renters and 19% of homeowners in North Carolina were considered housing cost-burdened, that is, spending 30% or more of their income on housing costs, according to the NC Justice Center.

Over the last two years, the median price of a home in North Carolina rose roughly 25% in 2021 and an estimated 5% in 2022. Also, the state has 347,275 extremely low-income renter households, but only 156,365 rental units considered affordable for those families. The NC Budget & Tax Center estimates that North Carolina could see the gap between housing units and residents’ need grow to 900,000 units by 2030.

North Carolina is hardly alone in this housing crisis. U.S. Census Bureau data shows that 40% of renters nationwide meet the definition of cost-burdened. From 2019 to 2022, the average price of a home in the United States rose from $391,900 to $543,600, a 38% increase.

The reasons for this affordability crisis are myriad and complex.

Looking specifically at North Carolina, and going back decades, the state has seen a huge increase in urbanization. Just 60 years ago, jobs were not concentrated in the urban core, but in smaller communities across the state, with cotton mills and less-mechanized agriculture serving as primary drivers of employment in the state. Losses in textile and agricultural employment, combined with the explosion of high-tech industries and the rise of concentrated professional service jobs, has caused North Carolina’s largest cities and the surrounding areas to see a majority of job and population growth in recent decades.

Those changes in the state’s economy began in the 1960s and accelerated in the 1980s, but they have continued to mean that land prices—which typically dictate the size of home that homebuilders construct—have risen fastest closest to the urban core.

The more recent surge in home prices has been driven by other factors, including cyclical building supply price increases and pandemic-related supply chain disruptions. According to the National Association of Home Builders, building material prices have risen more than 35% since January 2020, with 80% of that increase coming since January 2021. Examples include exterior paint rising by 50% and gypsum by 22%. NAHB also reports that skilled labor shortages mean higher labor costs and an increase in the time required to build a home. Meanwhile, interest rate increases pushed the average mortgage rate to 5.9% in January 2023, the highest level since 2008, making home ownership more difficult.

In this already challenging landscape, the rise of corporate buying of homes for both short-term rentals, like AirBnb, and longer-term rentals, puts more pressure on housing costs.

Despite the complexity of the causes of the housing crisis, some critics have sought to shift heavy blame to local governments, and their land-use policies and building approval processes. These critics typically don’t reveal that academic studies examining land-use reforms enacted to create more density have shown, at best, modest results when it comes to improving housing affordability.

LOCAL GOVERNMENTS RESPOND

Among local officials who work in the field of land-use planning and building approvals, there is a clear recognition that housing costs are rising faster than the wages of most residents. Many of those professionals cite the cost of land as making the development of affordable housing difficult, whether due to expected profit margins by builders and developers, or the financing required to develop the property.

Nonetheless, the NCLM/NCACC survey results of fast-growing communities show that many have begun answering the call to allow more dense development in response to the ongoing housing crisis.

Of the cities and counties responding, 60% indicated that they had revised zoning codes in recent years to allow more density by right. Nine of those cities, counties or joint jurisdictions responded that they now allow construction of residential units other than single family units in 75% or more of their residential zones. Also, 26 of the represented local governments, or 65%, indicated that they now allow accessory dwelling units (ADUs), or in-law suites, on single family lots.

Land-use reforms designed to encourage affordable housing have not stopped there. Thirty-five percent of responding cities and counties indicated that they had loosened parking requirements, decreasing the amount of land required to be dedicated to parking for residential development, while another 30% allow density bonuses for housing construction.

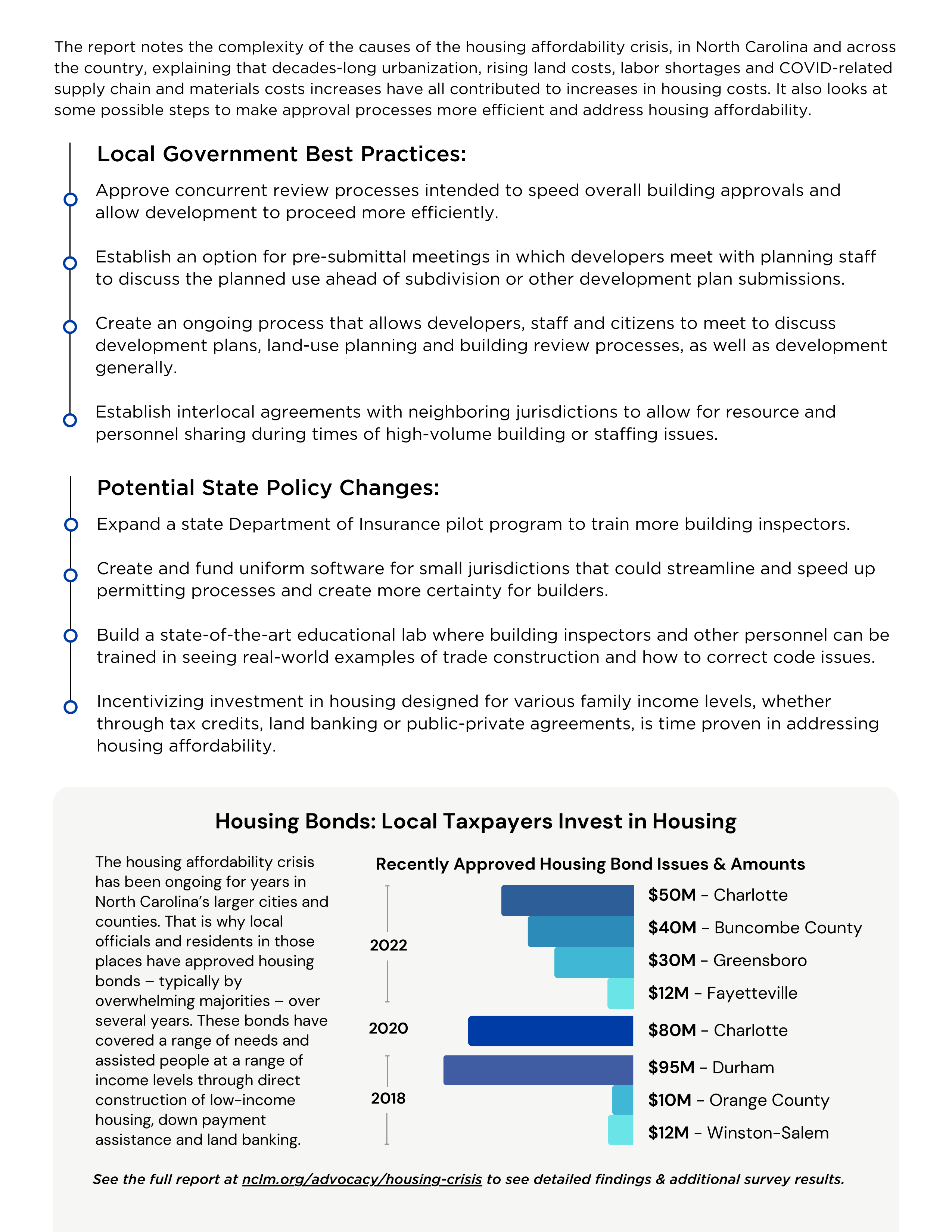

Residents in local jurisdictions across the state have also approved major bond initiatives in recent years aimed at infusing resources into various solutions aimed at increasing the stock of affordable and middle housing. (See “Housing Bonds: Local Taxpayers Invest in Housing.”)

Those efforts to increase density and pursue housing bonds demonstrate that local officials, both elected officials and planning staff, are responding. They desperately want to find ways to address housing needs.

Equally clear from the survey results is that these local government staffs do not see themselves as having adversarial relationships with developers. Asked to best describe that relationship, a full 75% of respondents said that they “generally enjoy a good working relationship” with developers, that the development community understands the constraints faced by staff, and that staff works to accommodate their needs. None of those surveyed characterized the relationship as “difficult.”

What is clear, though, is that growth can create tension among residents. Fifty percent of respondents said that residents have differing views about growth, depending on the development or project, while 22% reported palpable tension between those favoring and opposing development.

CONCLUSION

Communities across North Carolina clearly are grappling with housing affordability, and local officials have been at the forefront in attempting to find solutions to a complex and difficult challenge.

Given the complexity of the problem, no single magic wand can be waved that will suddenly produce more affordable housing.

What North Carolina can do is attempt to build upon and bolster the successes that are already working, and recognize that, when it comes to building approval processes, streamlining though technology and investing in human capital are likely to produce the most noticeable improvements.

Local governments do have the ability to look to their neighbors and determine best practices that are creating better results for homeowners, developers and the larger community.

Local government best practices include:

- Approve concurrent review processes intended to speed overall building approvals and allow development to proceed more efficiently.

- Establish an option for pre-submittal meetings in which developers meet with planning staff to discuss the planned use ahead of subdivision or other development plan submissions.

- Create an ongoing process that allows developers, staff and citizens to meet to discuss development plans, land-use planning and building review processes, as well as development generally.

- Establish interlocal agreements with neighboring jurisdictions to allow for resource and personnel sharing during times of high-volume building or staffing issues.

At the state level, a focus on how to put more people into the building inspections profession, or conversely, assisting them to be more efficient, would ameliorate a key concern of builders.

Potential state policy changes that could accomplish those goals:

- Expand a state Department of Insurance pilot program to train more building inspectors.

- Create and fund uniform software for small jurisdictions that could streamline and speed up permitting processes and create more certainty for builders.

- Build a state-of-the-art educational lab where building inspectors and other personal can be trained in seeing real-world examples of trade construction and how to correct code issues.

- Incentivizing investment in housing designed for various family income levels, whether through tax credits, landing banking or public-private agreements, is time proven in addressing housing affordability.

Bringing together the expertise and experiences of everyone involved in housing, whether in the private, public or nonprofit sectors, would result in a better understanding of the causes of the housing affordability crisis and better solutions in addressing it. With that in mind, the creation of a legislative study committee, to meet over a period of months, would acknowledge the importance of housing affordability to the state’s economy and residents’ quality of life.

{kind=link}